From Packaging to Energy Infrastructure: The Shift the Market Is Missing

Inside Time Technoplasts's Q3 Earnings Report

The industrial packaging industry has traditionally been a scale-driven, low-margin business—built around products like drums, cans & bulk containers that serve chemical, pharma & industrial supply chains. Growth here tends to mirror underlying industrial activity, with limited pricing power and heavy dependence on raw material cycles. Efficiency, distribution reach and working capital discipline define winners, but structurally, it remains a steady—not exciting—space. This is precisely the lens through which companies like Time Technoplast have long been viewed: reliable, global but ultimately confined to the economics of packaging.

What the market is beginning to miss, however, is a quiet but decisive shift underway. Time Technoplast is increasingly positioning itself not just as a packaging supplier, but as a last-mile enabler of energy infrastructure—through composite cylinders for CNG and LPG, cascades for gas transportation & early investments in hydrogen storage solutions. These are not incremental extensions of packaging; they sit at the heart of India’s transition towards a gas-based economy. Below are the current business pillars of Time Technoplast:

As the share of such value-added, higher-margin products rises, the business is gradually moving from volume-led packaging to infrastructure-linked growth. The label may still say “packaging,” but the underlying business is evolving into something far more consequential. Ironically, the recent LPG crisis—triggered by supply disruptions—does not reduce the relevance of the business, but reinforces it. As India grapples with energy security and distribution challenges, the need for efficient storage and last-mile gas infrastructure only becomes more urgent. Let’s dive into Q3 earnings report of Time Technoplast.

The first thing that we generally look at the quartely results for Time Technoplast.

Time Technoplast had a solid growth in 9 month with a 11% rise in revenue, 15% rise in volume. They specifically called out the difference being due to drop in prices of raw material showcasing how core packaging business is linked to commodity cycles. What also stands out is the stronger growth seen in Composite segment.

Now, let’s focus on Financial Results for Time Technoplast

For YOY results, Sales grew by 13% with a stronger growth coming from overseas. EBIDTA increased by 17%, PAT by 25%. Value added products are growing stronger as well- now at 30% of total sales on 9 months. Overseas business has grown upto 36%. Overall, there is a increase seen in net cash from operating activity and debt has been reduced significantly this year.

The first question was on the value added products. Currently, over 9 month period, this is contributing at 30% of total revenue. The question is how do we see it moving forward from here.

Management expects the proportion of value added products to increase and reach around 35% in next 2 years. The margin for the categories is very clearly called out around 18% compared to 13.5% for standard products.

Second question is on recycling:how is it helping in the margins of the business?

Time Echotech is a subsidary of Time Technoplast created that works on recycling and on its own is expected to maintain a 20% ROCE. For Time Technoplast standalone basis, the recycled material helps in cost reduction and long term compliance and more importantly, reduce reliance on external stakeholders.

There was a question on the flexible IBC business, the upcoming acquisition of Ebullient Packaging- details on the growth roadmap ahead.

Overall, management claims flexible IBC is a huge market. There is an in principle agreement on the deal. Ebullient packaging are a 250 cr annualized business with growth expected to be 25-30% ( stronger than traditional packaging). They also have higher revenues coming from exports.

There was a question on the prospect of Hydrogen cyclinders & its application in drones.

Management confirmed hydrogen cylinder and work with drones is still in early phases. They have no intention of making drones but are partnering with a drone company to test the viability of hydrogen cylinders. they expect commercialization to start next FY as the plant is commissioning from March’26.

The next question is on the expansion plans wrt Infrastructure vertical ie PE pipes and the demand sentiments seen in country.

Management confirmed today there is already 70% capacity utilization leading to a ceiling of revenue to a max of 450 cr for PE pipes business. Management is expecting infra development esp wrt smart city developments and hence, are looking to expand their capacity in Odisha. However, capacity is expected to kick in FY’28. Till then, scope for growth in this business is expected to be max of 20%.

The next question is around projected PAT growth for Time Technoplast.

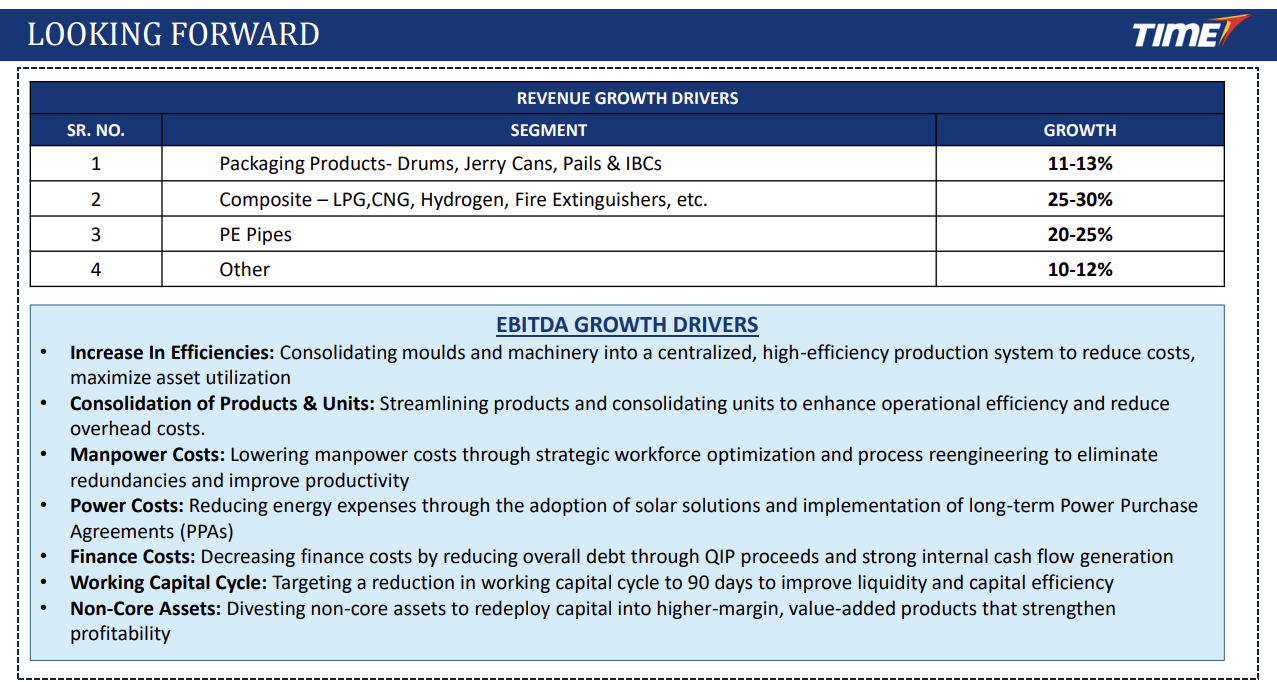

Management confirms with a volume growth of 13-14%, an EBIDTA growth of 18% and PAT growth of 25% is expected. Management confidence also comes from reduced interest cost because of lack of debt. They are also confident of 3 year plan ahead including drivers for growth of margin and revenue. Picture on Growth drivers for Margin below for reference:

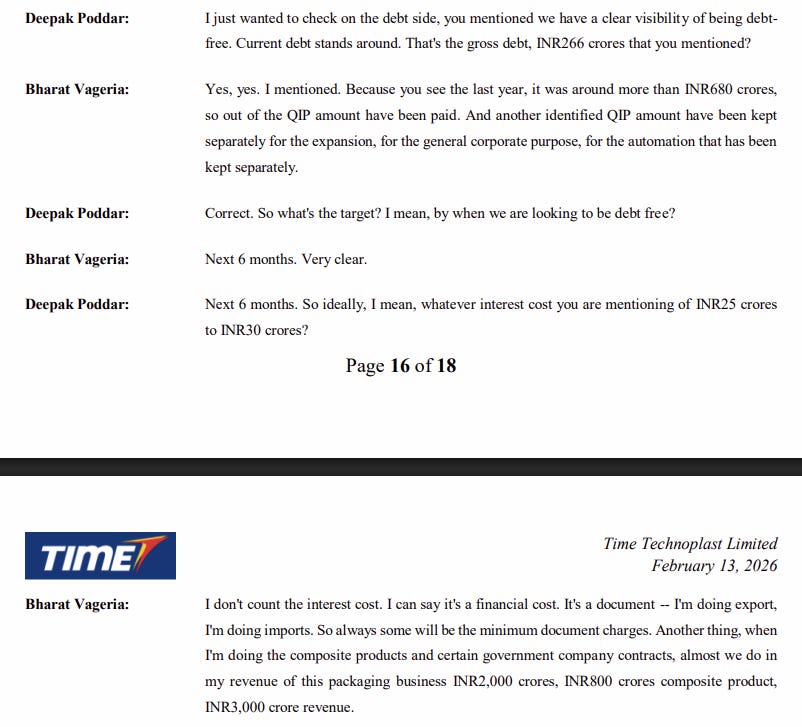

The final question is on the debt status of the company, when is Time Technplast targeting to be debt free.

Management has reduced its debt levels considerably from 680 cr to 266 cr this year. They target to be debt free in 6 months time. There will be small financial cost especially around document charges but the interest costs will be reduced by around 60 crores per year.

Overall, Time Technoplast story is interesting: what looked like a steady packaging business on the surface is quietly turning into something else.

Beneath the stable volumes and commodity-linked revenues, management is redesigning its earnings engine—through product mix, balance sheet discipline and cost levers. The shift isn’t loud but it’s consistent—and that’s what makes it interesting.

Here are 5 key take aways from what we read today:

Growth in business is stronger than it appears today backed with a healthy volume growth shocasing strong underlying demand.

Business mix is quietly shifting with increasing focus on Value-added products leading to a structural margin uplift

Earnings growth > revenue growth is core sign of any strong business. Management is targetting EBITDA +17%, PAT +25%

Balance sheet is becoming a tailwind with Debt sharply reduced, targeting debt-free in 6 months.

Multiple hidden levers building together and will look to emerge in coming years. From Time Ecotech to growing Composites to promising hydrogen cylinder trials, Time Technoplast has found ways to try and transform its boring packaging business into something lot more promising in reality.